Hi Traders,

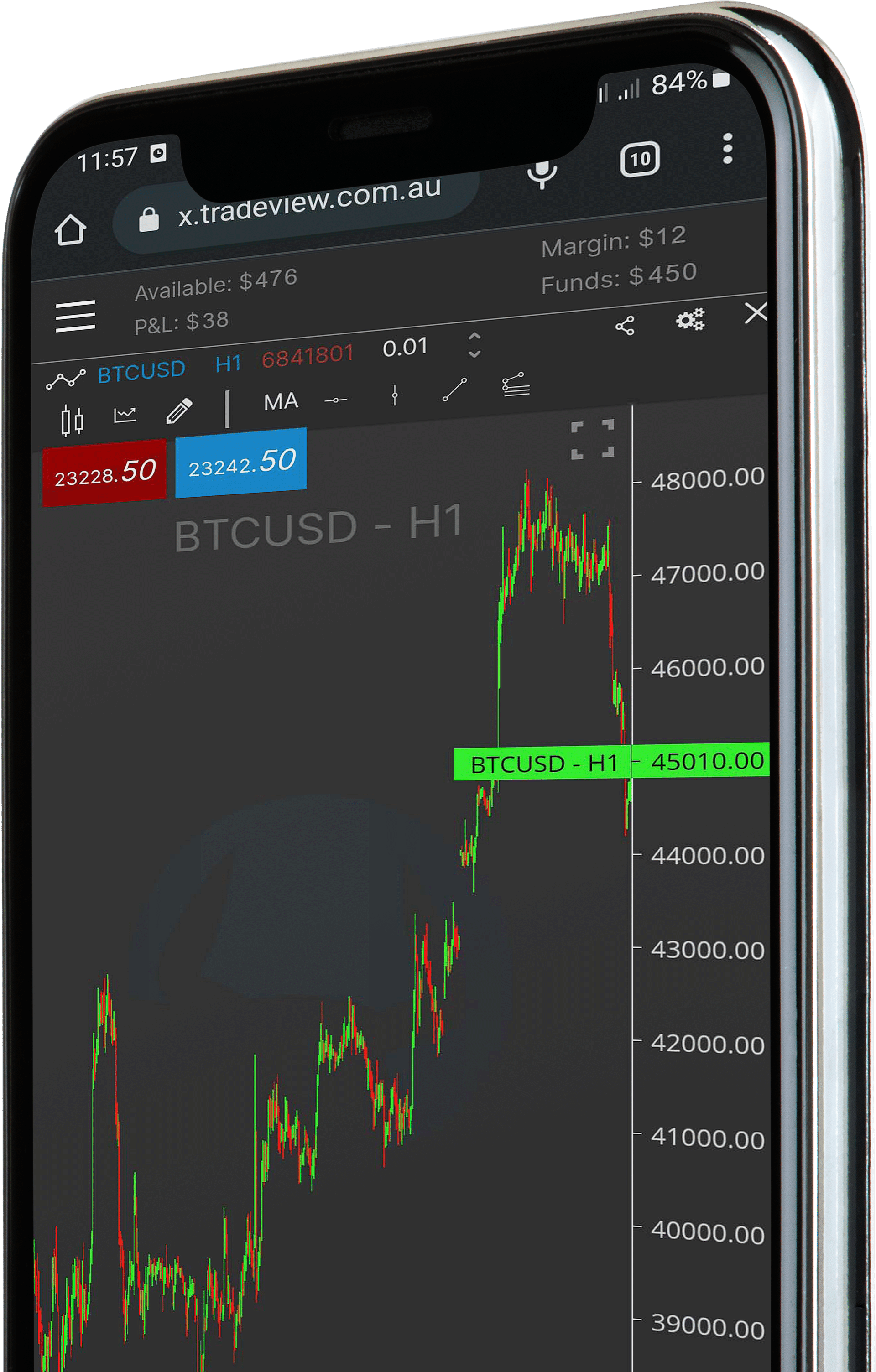

Today’s episode we will explore a real-life example sent in by a client, where their algo followed the rules perfectly, yet the trade outcome wasn’t ideal.

We all strive for that “picture-perfect” entry, and this case study highlights the importance of adding filters to further refine your trading model.

The Client’s Question:

Our client presented a trade setup where their algorithm executed a trade based on the defined rules. However, the trade lacked the optimal characteristics they were looking for. In simpler terms, the trade fit the criteria, but it wasn’t a “home run.”

Beyond the Basic Rules:

While establishing clear entry and exit rules is crucial, successful algorithmic trading often requires additional layers of filtering. These filters act as safeguards, preventing trades that might fall outside your desired parameters even if they meet the base requirements.

Exploring the “Entry Gone Wrong” Scenario:

The specific details of the trade setup will be revealed in the episode itself. However, let’s explore some general filtering techniques you can consider:

- Volatility Filters: Is the current market volatility conducive to your strategy? Adding volatility filters can help you avoid entering trades during excessively volatile or stagnant periods.

- Time of Day Filters: Does your strategy perform better at specific times? You can incorporate time-based filters to restrict trades to those timeframes.

- Technical Indicator Confirmation: Can another indicator add a layer of validation to your entry signals? Explore using additional technical indicators to confirm the strength of the initial signal.

Remember: Backtesting is key! Once you’ve implemented new filters, backtest your strategy on historical data to assess its impact on performance.

Why wait? Get started today. Sign up for an account today with the Tradeview Forex broker www.tradeview.tech and start creating your own automation.